AML Policy

1. GENERAL PROVISION

1.1. This anti-money laundering and counter-terrorist financing policy (hereinafter – the Policy) shall govern the implementation of anti-money laundering and terrorist financing measures by Bank of Central Limited (hereinafter - the Company).

1.2. This Policy shall apply to all employees of the Company and other persons, or entities associated with the Company.

1.3. The purpose of this Policy is to set the principles and define framework of the Company processes, procedures and systems aimed to identify, prohibit, and prevent activities of possible money laundering and financing of terrorists.

1.4. The Policy also serves as means of informing the Representatives of the Company of the applicable laws of Commonwealth of Dominica (hereinafter – Dominica) preventing money laundering and terrorist financing.

1.5.The Policy is in line with the national regulation of Dominica and further extends to applying and complying with international Standards on Combating Money Laundering and Terrorist and Proliferation financing CFATF 40 Recommendations and Special Recommendations on Terrorist financing, the CFATF Standards on AML Principles and best international banking practices on combating money laundering and terrorist financing.

2. CUSTOMER DUE DILIGENCE

2.1. It is essential for the Company to know the identity of the customer to whom it provides payment services, which explains why the Company follows the principle “know your customer”. To this end, the Company must take all relevant, targeted, and proportionate measures to determine whether the customer is acting in his/her own name or is under control, and to identify the beneficial owner.

2.2. The Company shall always identify and verify the identity of the customer and the beneficial owner before a person:

- 2.2.1. Opens a business or personal account with the Company;

- 2.2.2. Engages in any other services the Company provides;

- 2.2.3. Enters into a business relationship with the Company, or

- 2.2.4. Conducts occasional transactions that exceeds the thresholds of international currency transfers, whether conducted as a single transaction or several linked transactions as described by the law of Commonwealth of Dominica.

2.3. The Company shall apply the customer and beneficial owner due diligence measures not only to new customers but also to existing ones on a risk-sensitive basis in the event of new circumstances or new information related to the identification of the level of risk of the customer, beneficial owner, their identification data, activities and other relevant circumstances.

2.4.In all cases when identifying customer and/or the beneficial owner, the Company shall obtain information about the purpose of intended nature of the customer's business relationships.

2.5. Customer can be identified and verified remotely or being present in the office of the Company. The identity verification can be done by accepting such documents (the list is not exhaustive):

2.5.1. For legal entities:

- 2.5.1.1. Certificate of Incorporation or Registration;

- 2.5.1.2. Memorandum of Association or Articles of Association;

- 2.5.1.3. Shareholders Register/Certificate;

- 2.5.1.4. Directors Register/Certificate;

- 2.5.1.5. Proof of Address of the Company;

- 2.5.1.6. Certificate of Good standing;

- 2.5.1.7. License (if applicable);

- 2.5.1.8. Financial statements;

- 2.5.1.9. Organizational chart;

- 2.5.1.10. Source of Wealth (SoW)/Source of Funds (SoF).

2.5.2. For individual customers and/or Ultimate beneficial owners and Representatives:

- 2.5.2.1. Passport;

- 2.5.2.2. Proof of Address;

- 2.5.2.3. Source of Wealth (SoW)/Source of Funds (SoF).

2.6.Copies of all the documents submitted by the customer and information collected on the customer shall be kept in the customer's file (in electronic and/or hard copy format). Documents submitted by the customer to the Company in foreign languages may be accepted with a translator's certificate certifying that the translation from one language into another is true and the notary's certificate that the translator's signature is authentic, and, where the translation is bound together with a copy of the original document, with the notary's certificate certifying that the document is a true copy of the original.

2.7.Before establishing any relationship with the customer the Company must conduct sanction screening on the Customer (legal entity, direct/indirect shareholders, Ultimate beneficial owners, directors, representatives).

2.8.It is prohibited for the Company to establish business relationship with:

- 2.8.1. Shell Banks;

- 2.8.2. Companies that have Bearer shares

- 2.8.3. Individuals and/or entities residing in countries listed as prohibited.

- 2.8.4. an entity or individual listed as sanctioned individual/entity in international sanctions lists:

- 2.8.4.1.The UN Security Council resolutions;

- 2.8.4.2. The EU Consolidated list of restrictive measures;

- 2.8.4.3. The sanctions administered by the US Office of Foreign Assets Control (OFAC).

2.9. Before establishing business relationship, the Company also must identify Politically Exposed Persons (PEP's). It is a private individual who is or has been entrusted with prominent public functions. It includes the immediate family members, or persons known to be close associates of such individual. The Company understands that providing financial services to such individuals might pose higher money laundering risks therefore customers identified as PEP's require enhanced level of due diligence and the Company keeps the right to ask additional documentation in relation to political status of mentioned individuals.

3. ONGOING CUSTOMER DUE DILIGENCE

3.1. In all cases, the Company must conduct ongoing monitoring of the customer business relationship, including scrutiny of transactions concluded throughout the course of that relationship to ensure that the transactions being conducted are consistent with the Company's knowledge of the customer, its business and risk profile, including, where necessary, the source of funds. In order to ensure the appropriateness and relevance of the documents, data and information provided in the course of the customer and beneficial owner due diligence, the Company shall regularly review and update them. Periodic reviews are scheduled for all customers but may also be triggered by specific events.

3.2.Events that may trigger review in addition to the regularly scheduled review include the following:

- 3.2.1. material changes in the customer's profile;

- 3.2.2. the addition of a new product or account to a relationship;

- 3.2.3. the assignment of transfer of ownership of any asset (e.g., legal entity);

- 3.2.4. potentially suspicious activity detected by the transaction monitoring process.

4. CORRESPONDENT BANKING

4.1.When establishing correspondent relationships with other financial institutions the Company requires that the relevant financial institution applies appropriate due diligence measures, verification, and monitoring procedures of its clients.

4.2.After conducting relevant KYC procedures, the decision to establish correspondent relationships is within designated senior management officer of the Company.

4.3.The Company shall not enter or continue a correspondent banking relationship with a shell bank. Shell bank means a credit institution, or an institution engaged in equivalent activities, incorporated in a jurisdiction in which it has no physical presence, involving meaningful mind and management, and which is unaffiliated with a regulated financial group.

4.4.Furthermore, appropriate measures shall be taken to ensure that the Company does not engage in or continue correspondent banking relationships with a bank that is known to permit its accounts to be used by a shell bank.

4.5.Furthermore, appropriate measures shall be taken to ensure that the Company does not engage in or continue correspondent banking relationships with a bank that is known to permit its accounts to be used by a shell bank.

5. REPORTING SUSPICIOUS ACTIVITY

5.1. The Company shall promptly inform local Financial Services Unit (hereinafter – FSU) in Commonwealth of Dominica if it knows or has a reasonable ground to suspect that money laundering or terrorist financing is being or has been committed or attempted.

5.2.It shall be prohibited to disclose to the customer or other persons that information on the monetary operations carried out or transactions concluded by the Customer, or an investigation conducted in respect of them has been submitted to the Financial Services Unit.

6. RECORD KEEPING

6.1.In accordance with AML & CFT Program Record Retention, client identification records, new business and financial transaction records should be kept for a period of not less than seven years following the termination of a business relationship. Where necessary, these records may be kept for a longer period where investigations are ongoing, and circumstances predate this period.

6.2.All records must be kept in sufficient form to permit reconstruction of individual transactions to provide necessary evidence for potential prosecutions. The Guidance Notes permit that records can be retained in a format, including microfiche or other accessible computerized form, that would facilitate reconstruction of individual transactions (including the amounts and types of currency involved) within a reasonable time, so as to provide, if necessary, evidence for prosecution of criminal activity and to enable licensees to comply swiftly with information requests from the FIU. This applies whether or not records are stored off the premises of the licensee.

6.3.The Money Laundering (Prevention) Act provides that covered financial businesses shall keep business transaction records of all business transactions for a period of seven years after the termination of the business transaction recorded. The Proceeds of Crime Act prescribes, in general, a seven-year period. AML & CFT Program states that it is to be followed as best practice unless the laws of a particular country are more stringent. Since the AML & CFT Program is more stringent, in this case, the record keeping requirement of seven (07) years should be adhered to for all records.

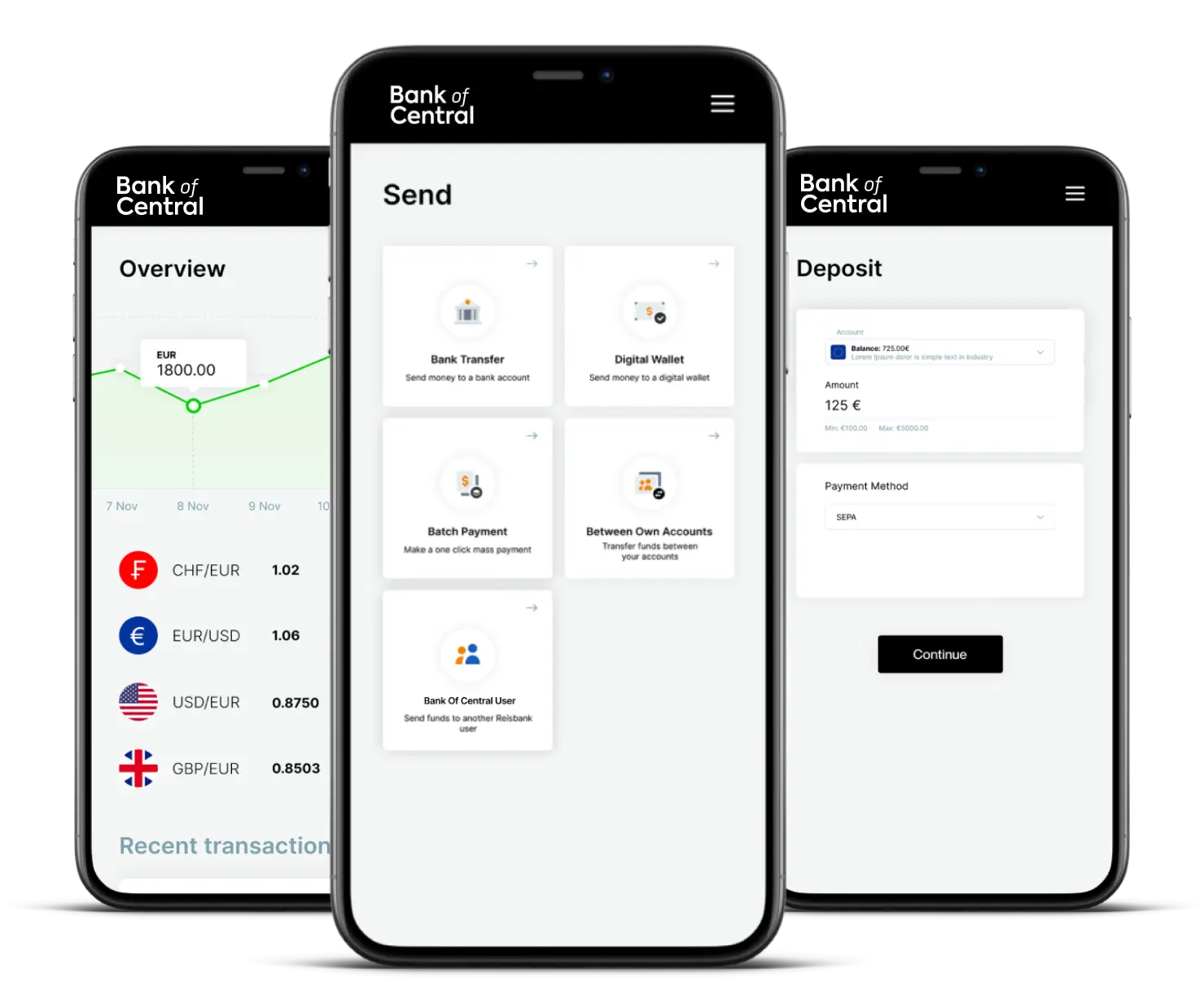

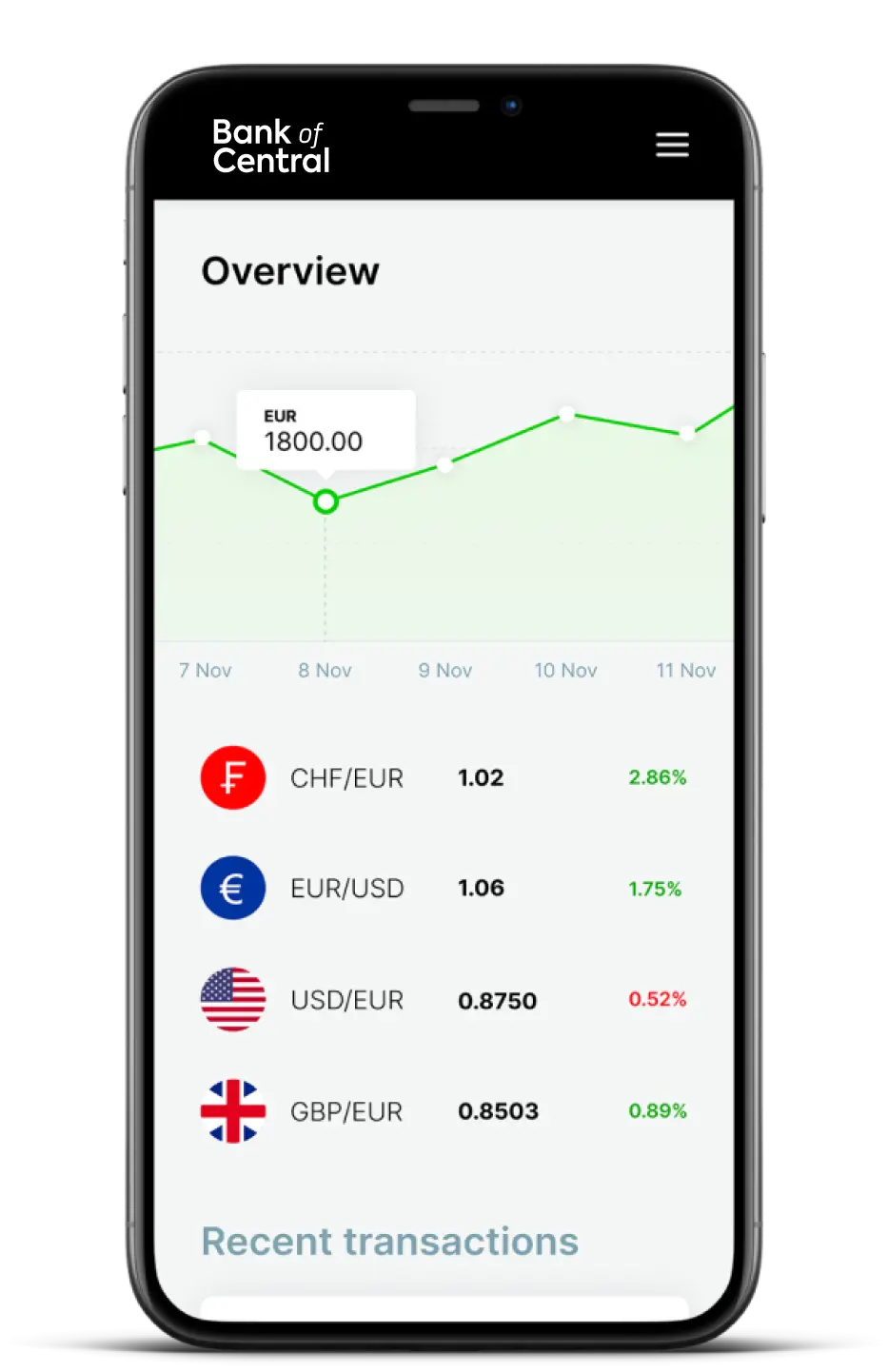

Take full control of all banking transactions

Control your own money, become an investor!

Manage different currencies freely

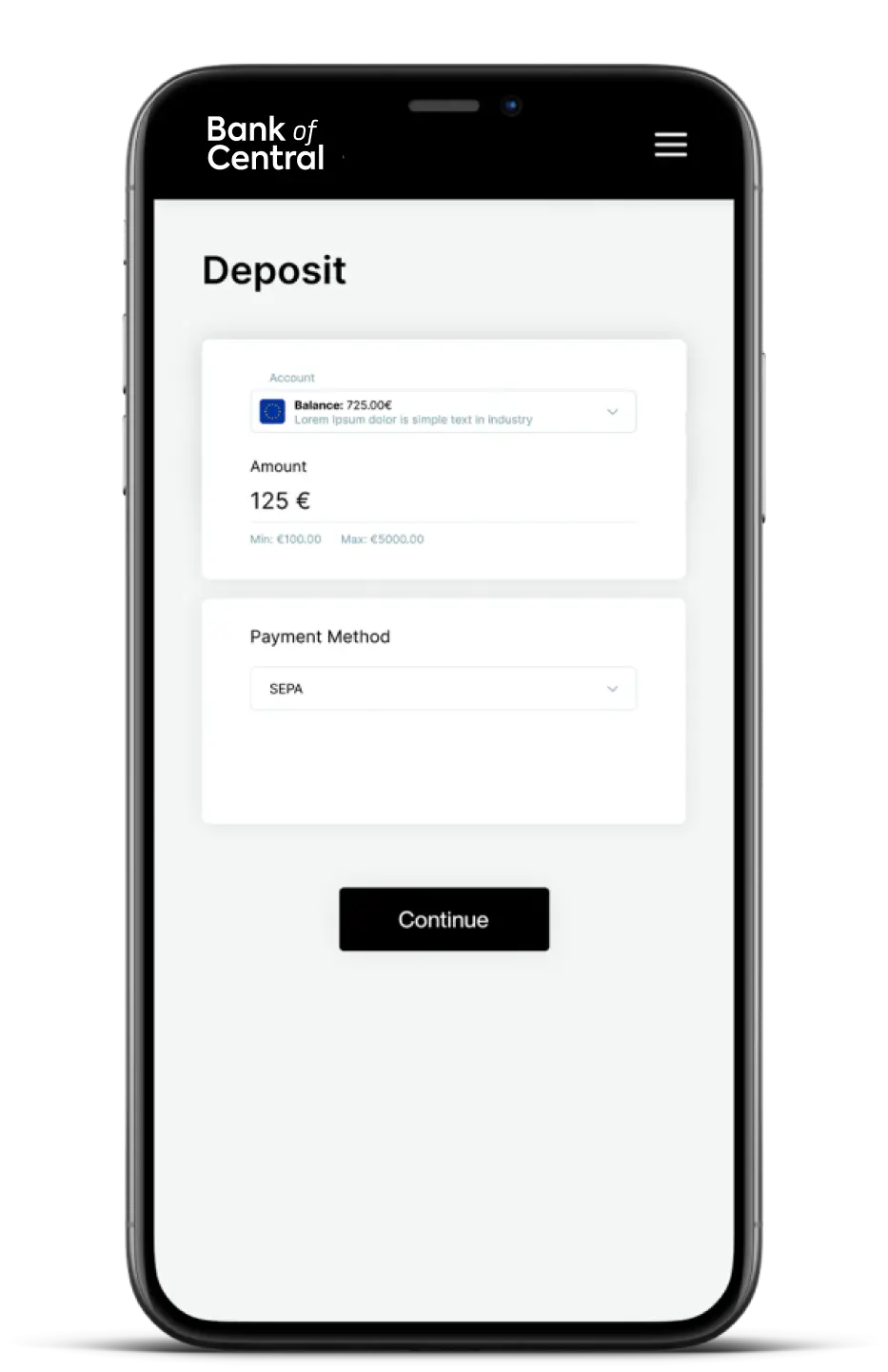

Deposit freely on the go

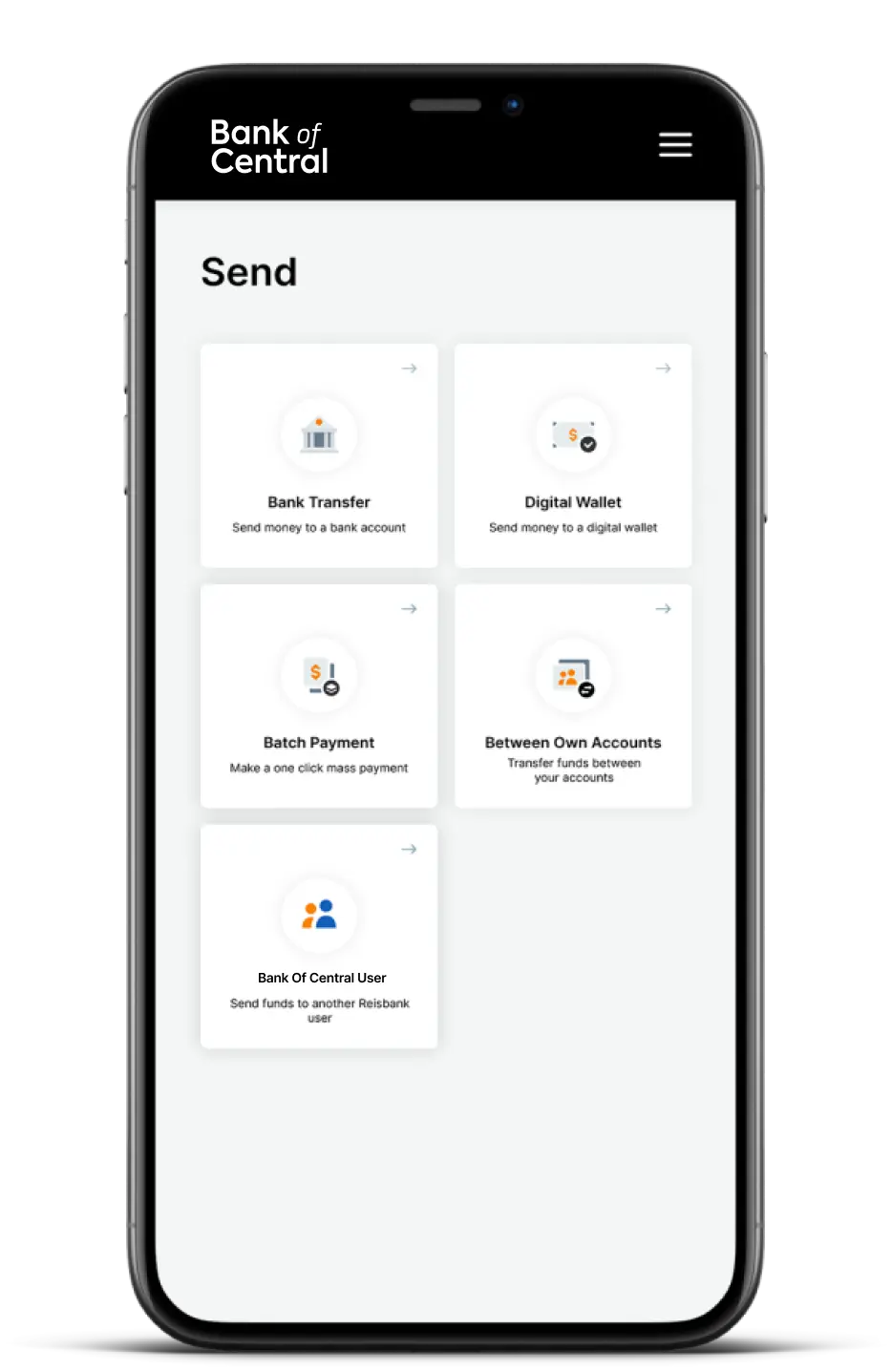

Send and receive cash fast and free of charge with Bank of Central

Manage different currencies freely

Fast and secure money transfers

Get in charge of your own investments